|

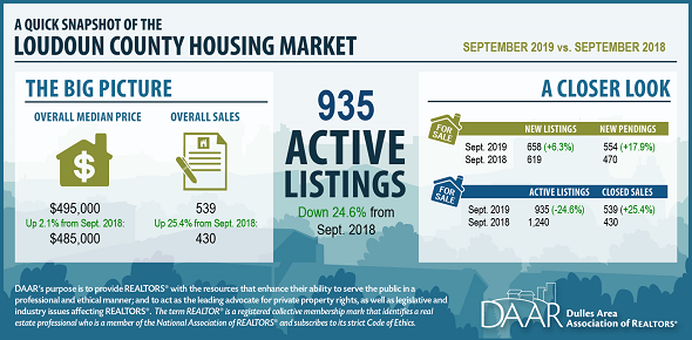

There's no doubt about it, the real estate environment is in a different place today compared with a year ago, but is it a bad thing? If we take a look back, the dreaded COVID years of 2020 and 2021 created an unexpected boom in our industry, to put it lightly. In early 2020, when masks and lockdowns and latex gloves and shoe covers were de rigueur, we all assumed that our businesses would come to a grinding halt, however, in Virginia, real estate brokers were deemed an essential service and we were allowed to continue to do business. Gradually, but pretty quickly, we saw folks packing up and moving away from big cities in search of open space and fresh air. As a consequence, property prices began to escalate while mortgage rates tumbled to record lows in the 2.5% region. It seemed that these increasing home prices did not deter buyers, in fact for two years, most properties listed at then realistic prices went under contract within days, and following multiple offers with increasingly escalating offer prices but with correspondingly fewer, if any, contingencies. We have all witnessed the significant rise in inflation which has caused mortgage rates to more than double in just a few months, meaning that buyers' affordability has been dramatically reduced. So here we are, with a market which has corrected, yet prices are still far higher than they were two years ago, and inventory remains very low. For buyers and their agents, respite is here because they are no longer fighting to win with their offers against multiple other offers, waiving important contingencies such as home inspections and well and septic. The panel below, courtesy of the Dulles Area Association of REALTORS®, provides a nice snapshot as to the market position in Loudoun County as compared to one year ago, however it's particularly helpful to look back three years, to 2019 (second panel below), to get a more realistic comparison. What we see here is a drastically lower inventory (660 listings -v- 935 in September 2019), and a median price today of $639,995 compared with $495,000 in September 2019.  September 2022 Market Snapshot  September 2019 Market Snapshot This lack of inventory in a market where there is a high demand for property is fuelling a continued healthy market, but with rates at around the 7% mark, we are seeing more negotiation, longer time on market and, happily, we are back to a position where buyers are able to properly do their due diligence with home inspections, well and septic inspections and retaining financing and appraisal contingencies.

0 Comments

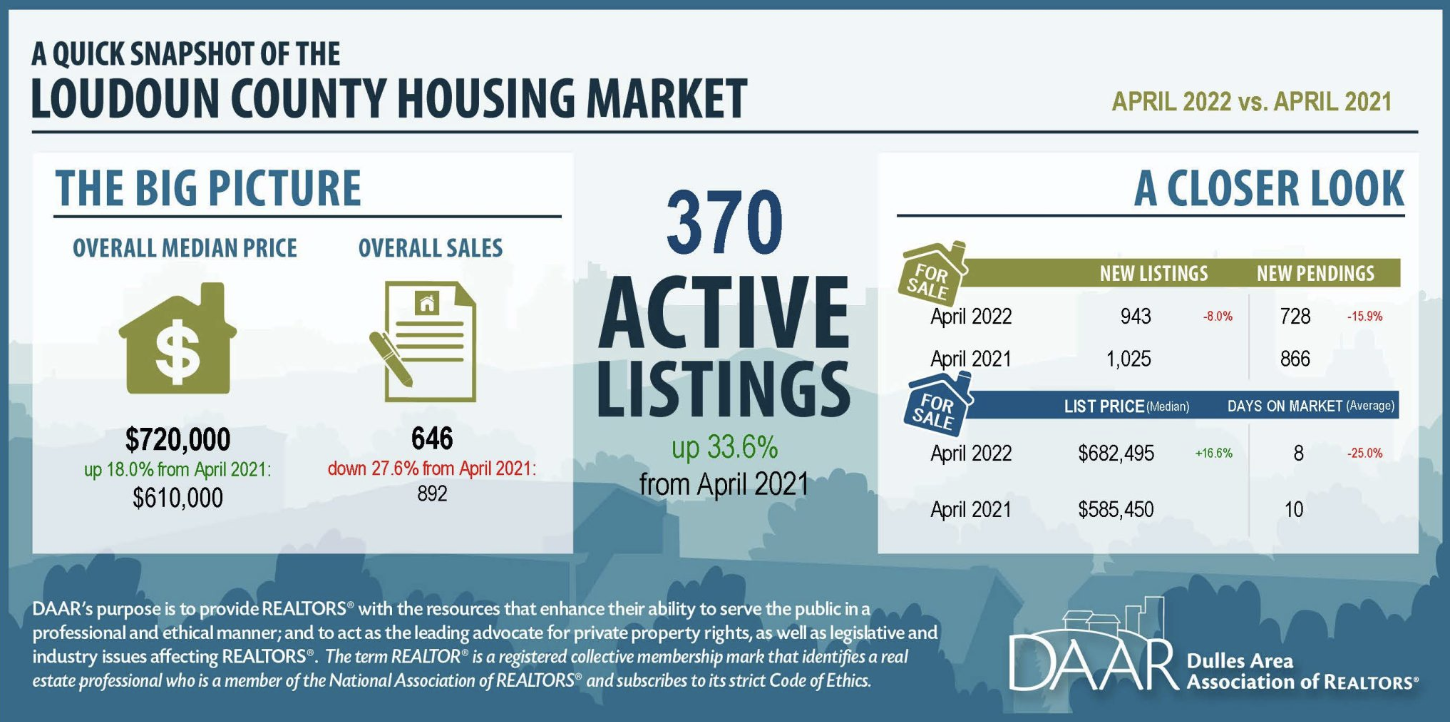

The Dulles Area Association of Realtors® monthly market indicators report for April 2022 is now available, providing both a snapshot and further in depth detail in to our local real estate market.  Courtesy Dulles Area Association of REALTORS® Active listings are up significantly year over year (YoY) at 370 listings, or 33.6% more YoY, nevertheless new listings are 8% lower than the same time last year. The median list price continues to increase, 16.6% for the year to a new level of $682,496, however the median sold price is now at $720,000 compared to $610,000 in April 2021, based on 27.6% fewer sales YoY.

The latest Home Demand Index for the Washington DC region, researched and prepared by Bright MLS, can also be reviewed here. The local, and in fact national real estate market has seen record upward movement in sales prices and volume since the start of the COVID-19 pandemic. Our market here in Loudoun County and Northern Virginia is no exception as recently released quarter 4 2021 versus the same period in 2020 reveal.  Courtesy of the Dulles Area Association of Realtors As we have all seen, inflation is at a 40 year high at 7.5% which is expected to decrease later in the year, but it's certainly a concern.

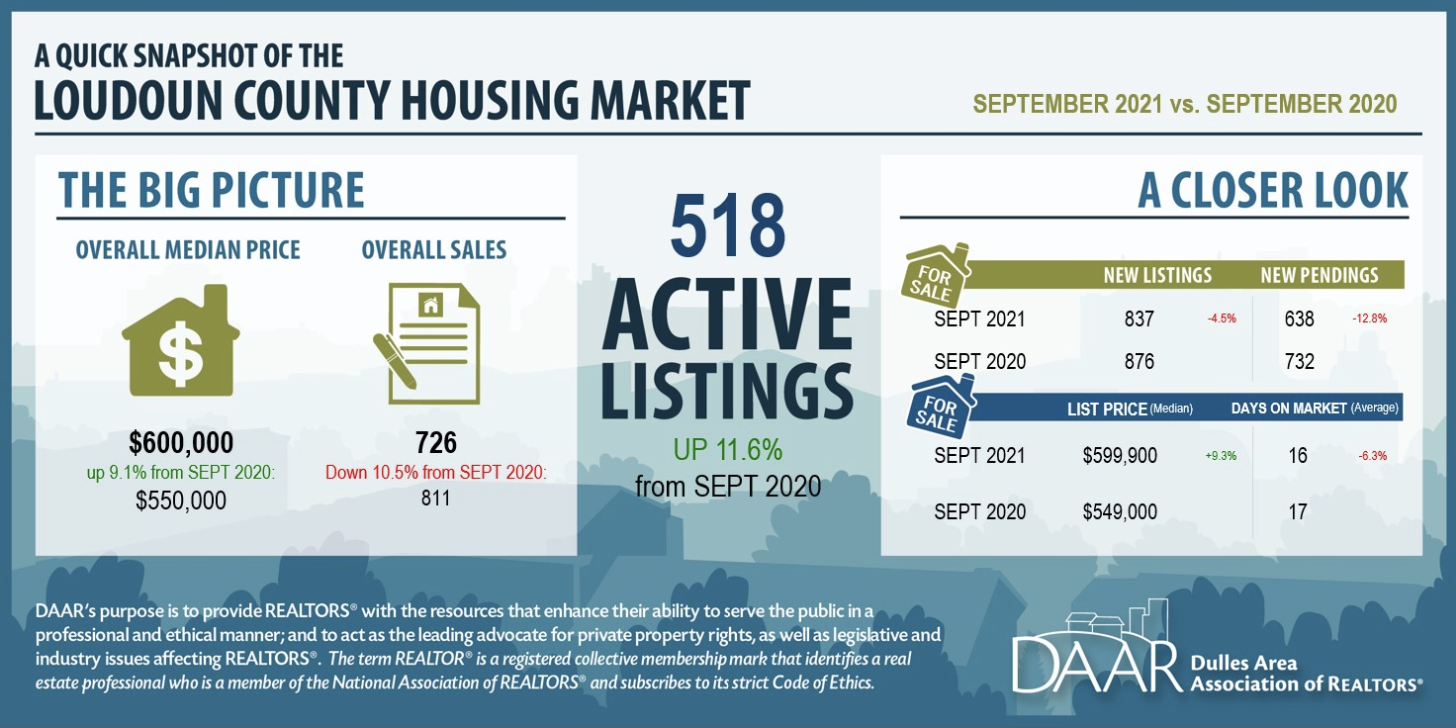

Interest rates are on the rise and indicators are that mortgage rates could be 1% higher than they are today by summer. That's relatively significant but would still be in the 4's, well well below what we were used to not so many years ago. For the full report, click or press HERE and as always, don't hesitate to give me a call, text or email for more information. Peter n.b. thanks to the Dulles Area Association of Realtors, of which I am a board member, for these well researched figures The market is showing signs of returning to something like a more balanced one. While September sales in Loudoun County were down 10.5% YOY, when compared to 2019, it is stronger. What does this all suggest? Perhaps that buyers who were shut out will now return to the market, while sellers will still experience strong returns in short timeframes. Win-win. Key is still price, condition and location. There’s no getting around that maxim. Yet prices have been moving up continually, and the report demonstrates that, showing overall median prices up almost 10% as compared to September 2020.  Mortgage rates have been inching up, primarily thanks to inflation concerns, but are still at extremely low levels. To paraphrase my friend and loan officer, Tan Tunador with ACM (Atlantic Coast Mortgage), "They [rates] are still near historic lows (remember the 6,7,8 or even over 10% rates?). Once the consumer gets the sub-3% rates our of their minds the low 3s will be the new normal again."

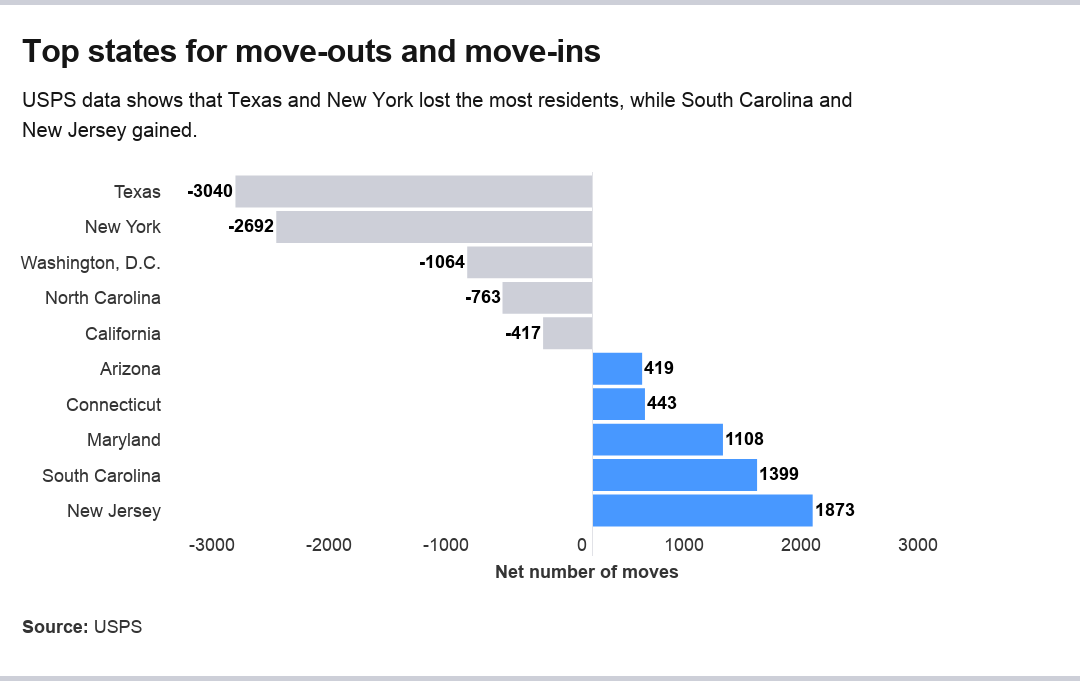

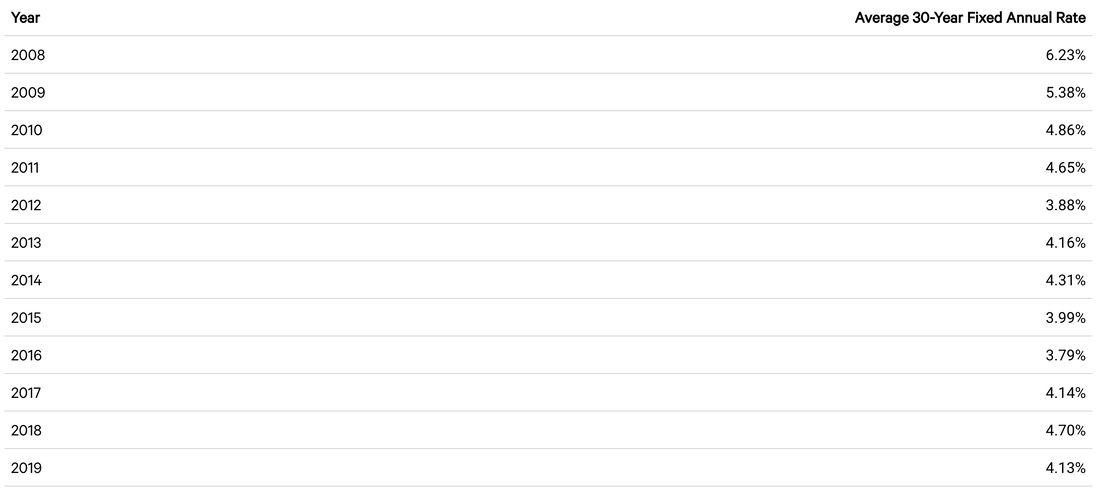

Check out the the full report by clicking/pressing on the image above, and have a great day! Peter The coronavirus pandemic has dramatically changed the way we live, and as a result, new trends are emerging around where, exactly, we want to call home. United States Postal Service mail forwarding data from January through mid-September 2020 shows that many in the nation’s cities moved to suburbs, presumably in search of more space while so many of us are working from home. New York City saw the biggest population shifts of any city in the country, and Texas had the most movement as a state, driven by people leaving the downtown cores of Houston, Dallas and Austin, mostly for nearby suburbs.  If you are looking to move to the city, right now is a great time to buy in downtown city neighborhoods, because prices there are holding steady or even declining a little as competition for housing in suburbs heats up. Coupled with historically low mortgage rates, there are good deals to be found that could give you a great return on investment when cities reach their new post-pandemic equilibrium. Keep in mind that lots of cities have more public health restrictions in place than less-dense areas, so make sure you know the municipal rules before you plan to move. If you are looking to move to the suburbs or away from a city center, be prepared for the aforementioned competition. You’ll want to do everything you can to make yourself an attractive buyer, so get preapproved for your mortgage and be ready to act fast when you find a house that’s the right fit. Keep in mind that prices in the suburbs have been going up as demand has increased and supply has stagnated, so it may be harder to stick to your budget. You need to be prepared to walk away from a house you may love so you don’t wind up with a bigger mortgage than you can afford. What is a 30-year fixed mortgage?A fixed-rate mortgage has an interest rate that doesn’t change over the full term of the loan, which, for a 30-year mortgage (as the name suggests) is 30 years. It’s a popular choice for many homebuyers because of its stable monthly principal and interest payments ideal for predictable monthly household budgets, at a more affordable cost than shorter-term loans. Historical 30-year ratesAccording to Freddie Mac historical data, the 30-year fixed rate shot up to about 18 percent in September and October of 1981, which would give current homebuyers quite the sticker shock. The U.S. was in the midst of an economic recession back then, and the Federal Reserve hiked rates in an effort to curb inflation. Today, mortgage rates are near historic lows, hovering around 3 percent. Knowing where rates have been — and what drives them — can help you put things into perspective as you evaluate loan offers. When the housing crisis hit in 2008, the average annual 30-year fixed rate was 6.23 percent, according to historical Bankrate data. Since then, it has fallen considerably. When 30-year fixed mortgage rates decline, getting a mortgage is more affordable for homebuyers and those looking to refinance. However, home-prices, which have been rising for the last several years, can present a barrier for potential homeowners even when mortgage rates are low. The benchmark 30-year fixed rate hit a record low of 3.03 percent during the week of Oct. 28, 2020, according to historical Bankrate data. Bankrate average annual 30-year fixed mortgage rate, 2008-2018 When to consider a 30-year fixed mortgageChoosing the right home loan is an important step in the homebuying process, and you have a lot of options. You need to take several factors into consideration, including your credit score, income, down payment amount, budget and financial goals. Here are the main benefits and drawbacks of a 30-year fixed mortgage. Pros of a 30-year mortgage

Cons of a 30-year mortgage

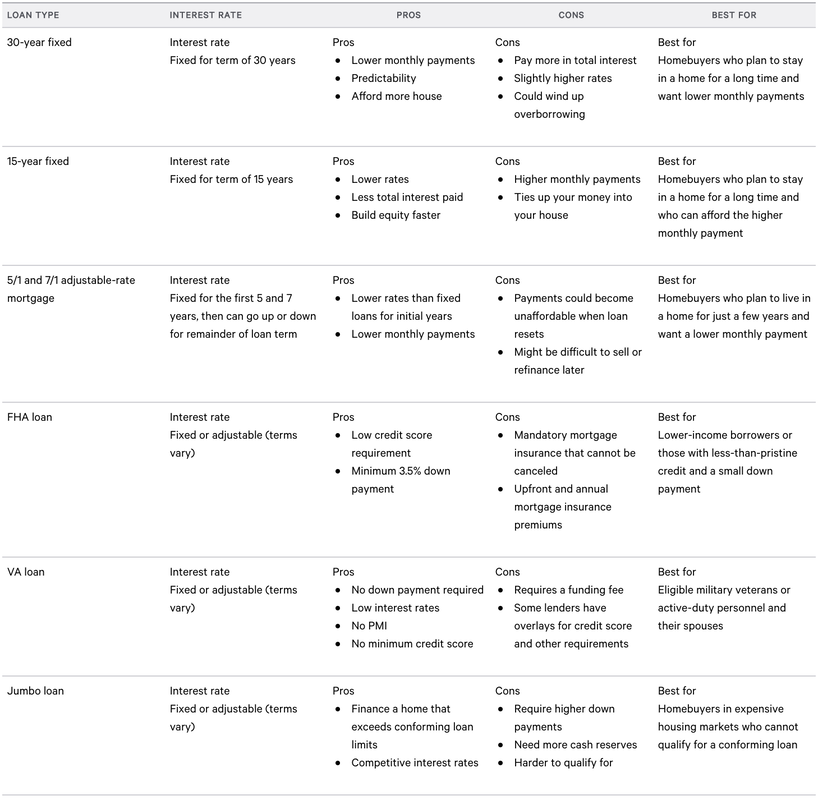

Is a 30-year fixed mortgage right for you?Choosing the right home loan is an important step in the homebuying process, and you have a lot of options. You need to take several factors into consideration, such as your credit score, income, down payment amount, budget and financial goals. Here’s how a 30-year fixed mortgage stacks up against other loan types.  Refinancing a 30-year mortgageIt’s generally a good idea to refinance your 30-year fixed mortgage into a new loan if you can get a lower interest rate, lower monthly payment, or improve your financial situation in another way. However, if you’re several years into repaying your loan and you refinance into a new 30-year mortgage, you’ll be paying more total interest in the long run by starting the repayment clock from scratch again. You’ll also need to determine if the closing costs on your new loan outweigh the savings you’ll gain from lower monthly payments over time. When you refinance a 30-year mortgage, you’ll pay lender origination fees and third-party fees for an appraisal and other closing costs. Most lenders also require you to have at least 20 percent equity in your home to refinance, so make sure you qualify before planning a new budget for yourself. Keep in mind that most mortgage refinances set to close on or after Dec. 1, 2020 will be assessed a 0.5 percent fee, which will make them slightly more expensive. Many lenders are already pricing the fee into their loan offers. The fee was announced by the Federal Housing Finance Agency earlier this year, and applies to all FHFA-backed loans valued at $125,000 or more. If you can, consider refinancing a 30-year mortgage into a shorter loan, which will avoid lengthening your repayment and save you on interest. Keep in mind, though, you might have a higher monthly payment depending where you are in the amortization schedule. How do I view personalized 30-year mortgage rates?Use the tool at the top of this page to see what kind of rates are available in your situation. You just need to give us a little information about your finances and where you live. With that data, Bankrate can show you real-time estimates of mortgages available to you from a number of providers. Other mortgage tools:

|

AuthorPeter has written for his local magazines, Country Zest & Style and Middleburg Life as their Wine contributor. He also enjoys writing blogs on interesting and pertinent real estate matters, so please follow! Archives

June 2024

Categories

All

|

RSS Feed

RSS Feed

Peter Leonard-Morgan

|

© COPYRIGHT PETER LEONARD-MORGAN 2023. ALL RIGHTS RESERVED.

|

Sotheby's International Realty Affiliates LLC fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each Office is Independently Owned and Operated.